An insurance bond is a bond that is designed to function as a risk management tool. What does that mean and how does an insurance bond differ from an insurance policy? In this article, we explore those questions, look at how insurance bonds work and introduce surety and fidelity bonds.

What is an insurance bond?

An insurance bond is a bond that is designed specifically to protect an individual or organization against financial loss if certain circumstances occur, such as:

- the failure of another party to fulfill a contractual obligation; or

- their employee commits fraud.

A ‘bond’ is a written promise to pay or act if specific conditions are met; e.g., an event, or the passage of time. The type of bond that most of us are familiar with is the financial instrument that governments and corporations issue for the purpose of raising capital. These bonds are effectively loan agreements. The government or corporation is the borrower and the investors/bondholders are the lenders. These ‘financial’ bonds state the terms of the loan and the promise to pay interest and to return the principal at a specific time.

An insurance bond is also a promise to pay but it has a different purpose – to protect against financial loss or to guarantee compliance. The condition for payment is not the passage of time but rather, whether and when a specific negative situation occurs.

Insurance bond vs insurance policy

An insurance bond is a risk management tool, like an insurance policy. They are, however, not the same. The most obvious area of difference is in the contract structure. Let’s take a look:

Insurance policy

An insurance policy is a contract between two parties, the insured party, and the insurance company.

Insured party – the person or entity who is at risk of experiencing a covered financial loss and buys insurance to transfer the financial risk.

Insurance company – the company that agrees to take on that risk; assesses the probability of loss and combines many exposures together to pool the risk.

If the insured party experiences a covered loss, they file a claim with the insurance company which is then contractually bound to pay.

Example:

A contractor purchases professional liability insurance from an insurance company. Subsequently, the contractor is sued by a client who alleges the contractor made an error that cost the client money. The client wants to be compensated. The courts deem the contractor did not actually make an error. Even so, the contractor suffers a financial loss in the form of defence costs incurred. The contractor’s insurance company covers the loss.

Insurance bond

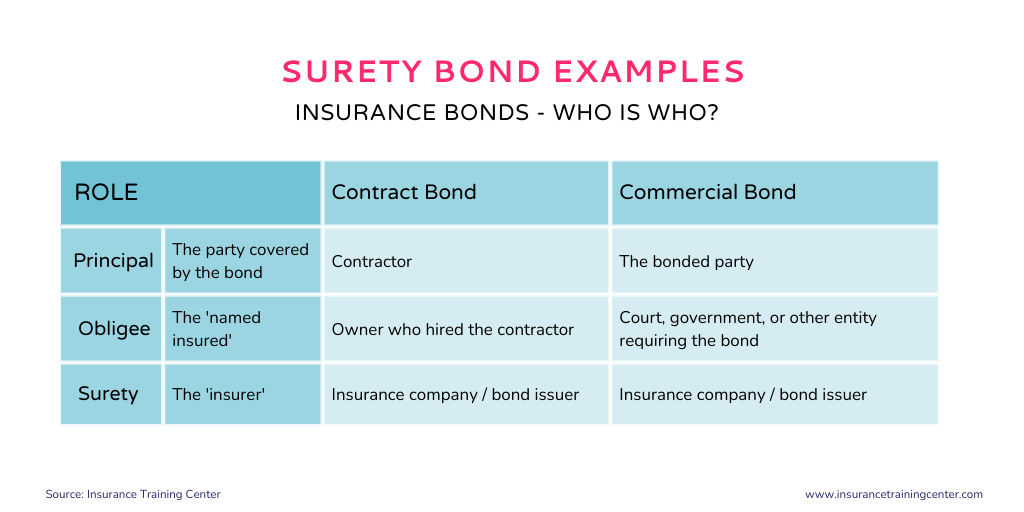

An insurance bond is a contract between three parties, the principal, the surety and the obligee.

Principal – the person or persons who are bonded and paying the bond premium. Their obligation is to complete the contract as promised, perform ethically as promised, etc. Also called the ‘obligor.’

Surety – the guarantor/bonding company; the person or entity that has agreed to vouch for the principal. They guarantee that the principal will fill their obligation and, if that does not happen, the surety promises to step in and make things right.

Obligee – the person or entity to whom the principal owes the obligation, the counterparty in the contract, their employer etc.

Example:

A construction company (the principal) purchases a performance bond from a bonding company (the surety), for a client (the obligee). The bond promises that, if the construction company does not complete the agreed project as promised in their contract, and the construction company is unable to pay, the bonding company will step in and pay an agreed amount to the client.

There are two main types of insurance bonds: surety bonds and fidelity bonds. The above example is a type of contract surety bond.

What is a surety bond?

A surety bond guarantees performance as contracted or provides security. The bond doesn’t protect the buyer of the bond (the principal) but rather a third party (the obligee) who is at risk of experiencing a loss.

There are many different types of surety bond. Here are some examples:

- Contract bonds – protect from loss due to non-compliance with the contract e.g., bid bonds, performance bonds, payment bonds, warranty bonds.

- Commercial bonds – guarantee compliance with law e.g., license and permit bonds, customs bonds, court bonds.

What is a fidelity bond?

A fidelity bond guarantees a faithful, loyal relationship with the purpose of protecting an employer or other entity from financial loss resulting from dishonesty and fraud, from criminal acts.

Here are some fidelity bond examples:

- Commercial crime fidelity bond – protect against employee dishonesty and fraud

- Financial institution bond – protect against employee dishonesty and fraud

- ERISA fidelity bond – protect against dishonesty and fraud by plan fiduciaries (read more about ERISA bonds)

- Public official bond – protect against dishonesty and fraud of a public official

Today, most (but not all) kinds of fidelity bonds function as insurance products, a contract between two parties, an insurer, and the insured. The commercial crime fidelity bond is a prime example of this. The term ‘bond’ in this case is a historical holdover from the days when individuals purchased ‘fidelity bonds’ from a third party to guarantee their trustworthiness to potential employers. That has evolved to become the Employee Dishonesty insuring clause (or fidelity coverage) in today’s commercial crime insurance policy.

Learn more about: Commercial Crime Insurance insuring agreements.

Where to get an insurance bond?

Only licensed surety companies can issue insurance bonds. Licensed sureties include specialized surety companies and many insurance companies. It’s wise to compare your options so contacting an insurance broker is a good place to start.

In Canada, surety licensing is provincial or federal.

Where can I learn more?

- Australia – Australian Surety Association – https://australiansurety.com.au/

- Canada – Surety Association of Canada – https://suretycanada.com/

- USA – The Surety & Fidelity Association of America – https://surety.org/

- International Credit Insurance & Surety Association – https://icisa.org/