Managing General Agents (MGA) help insurers and reinsurers to grow their businesses and expand into new markets. MGAs are not insurance companies yet they do some of the work of insurance companies. They are intermediaries yet they are not insurance brokers, rather, they support insurance brokers. So what are they? Where do they fit into the insurance industry landscape? And how do they bring value to insurers, brokers, and insurance buyers?

Read the following article to find the answers.

What is an MGA?

A Managing General Agent (MGA) is an agency that is contracted to perform various business functions, such as underwriting, binding, policy administration, claims, and distribution, on behalf of (re)insurance companies. Some MGAs specialize in a particular type of insurance or risk, for example: property, cyber, aviation, or construction. MGAs are different from insurance brokers in that the insurer has given the MGA the power to underwrite and perform various other tasks that would normally be performed by the insurer inhouse. Some MGAs are independent businesses, others, insurer-owned or broker-owned.

According to AM Best, there were 663 MGAs in the USA in 2020. And, at the time of writing, the Canadian Association of General Managing Agents and the UK’s Managing General Agents Association websites give member numbers of 65 and >300, in Canada and the UK, respectively.

What is delegated authority?

Delegated authority is at the core of the MGA business model.

The term ‘delegated authority’ refers to a contractual arrangement under which one party authorizes another party to act on their behalf. An insurer grants an MGA the authority to perform certain business functions on its behalf: underwriting, binding cover, claims handling etc. without having to obtain case by case approval from that insurer. These two parties have a ‘delegated authority relationship.’

AM Best talks about the “delegated underwriting authority enterprise” which it defines as, “a third party appointed by a (re)insurer, through contractual agreements, to perform underwriting, claims handling, and other administrative functions on behalf of its partners.” [1] The MGA is the most common form of DUAE. This category of insurance entities also includes Managing General Underwriters (MGUs), coverholders (term used in the UK, primarily with respect to the Lloyd’s market), and program administrators, among others. Note, it can be hard to distinguish the differences, and names are at times used interchangeably.

[1] AM Best Market Segment Report: Delegated Underwriting Authority Enterprises Gaining Market Traction, March 1, 2022.

How insurers use delegated authority

Entering a new market can require a significant investment, both in terms of money and time – dealing with local regulations, hiring staff, learning the market, putting infrastructure in place, etc. Delegating authority enables insurers to extend their reach into new geographies and specialized markets relatively quickly and with limited investment. MGAs are familiar with the business risks related to the specialized coverage they offer. They are better able to underwrite and price these policies than an insurer entering the market for the first time. Insurance companies enter into this type of outsourcing arrangement to test new products or markets, or when they consider doing so more cost effective or practical than keeping the work inhouse.

The extent, nature and parameters of the services that the MGA provides on behalf of the insurer are stipulated in the contract between the two parties known variously as a Delegated Authority or MGA Agreement.

What do managing general agents do?

The breadth and depth of MGA’s operations depends on the extent of the delegated authority granted by the (re)insurer. The insurer may also specify a particular line of business or set of insurance products. MGAs may contract to work for insurers and/or reinsurers.

The functions the MGA takes on may include, but are not limited to:

- Soliciting new business – promoting insurance products to customers, agents, and brokers, appointing retail agents;

- Underwriting risk – assessing, rating, and accepting or rejecting risk within pre-agreed parameters, pricing insurance policies

- Binding cover – committing the insurer to a new insurance policy, issuing insurance policies

- Policy administration – billing and collecting insurance premium, processing, servicing and renewing policies

- Claims management – investigating, processing, settlement claims, assisting with loss control

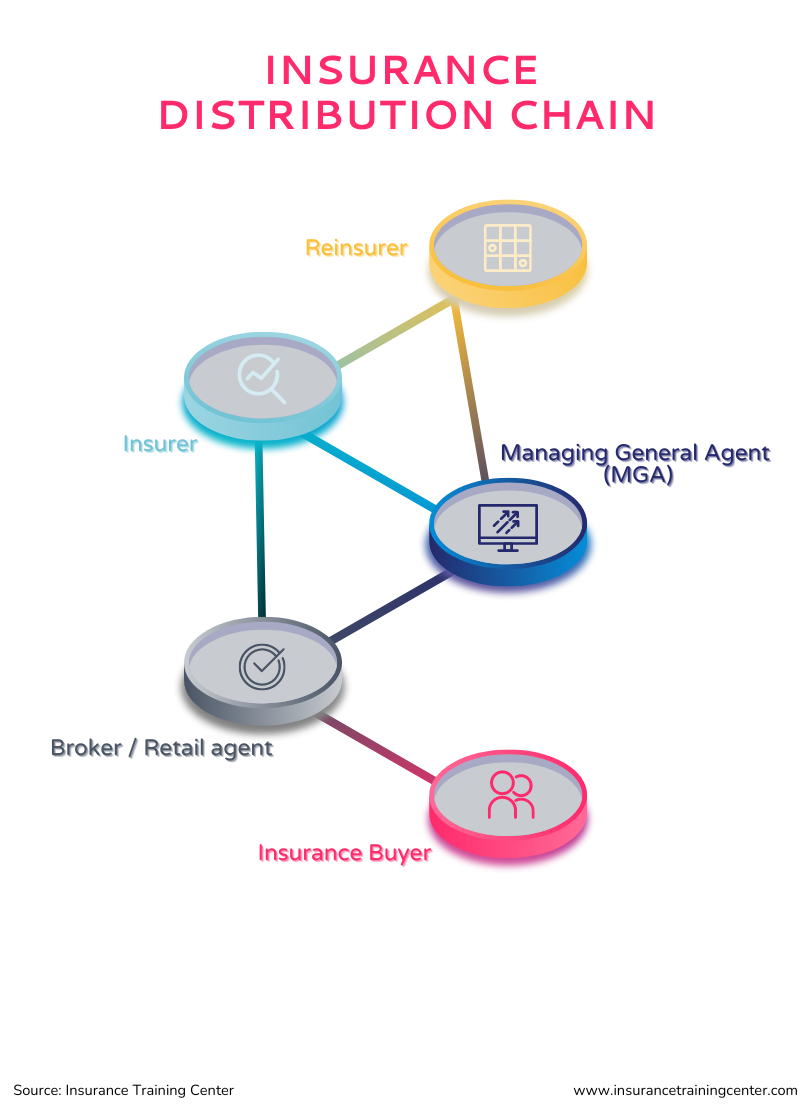

Where do MGAs fit in the distribution chain?

MGAs are intermediaries.

An MGA:

- acts as a distributor and outsourced service provider for both insurers and reinsurers.

- provides underwriting expertise, insurance cover, and related services

- to insurers on behalf of reinsurers; and

- to insurance buyers on behalf of insurers via insurance brokers and retail agents. While less common, MGAs may also support insurance buyers directly.

How do MGAs differ from brokers?

Insurance brokers work for the insurance buyer delivering professional advice, sourcing insurance solutions that meet the needs of the buyer, and providing ongoing guidance and support, through claims and policy renewal. While both MGAs and brokers are intermediaries, they are really very different. For example, MGAs work for the (re) insurer whereas brokers work for the insurance buyer. And because MGAs have binding authority from their insurance partners, they can provide a totally different set of services than can other intermediaries. The following chart provides more detail on the differences between MGAs and insurance brokers.

| Managing General Agent | Insurance broker | |

| Fiduciary duty | To the insurance company | To the insurance buyer |

| Industry position | Intermediary between the insurer and the broker | Intermediary between the customer and the MGA or insurer |

| Services provided | Underwrite, price, bind cover, collect premium, claims management and settlement | Advise clients; source and negotiate suitable insurance coverage, collect premium |

| Unique knowledge | May specialize in certain risks or market sector(s) | May have industry specialization but less common. |

| Compensation | Commission from the insurer on policies sold plus profit or loss of policies they have underwritten | Commission from the insurer on policies sold |

How MGAs add value

According to a 2022 survey by Insurance Business Canada, brokers use four key criteria when looking for an MGA: (1) responsiveness, (2) pricing, (3) ability to place niche risks, and (4) product range. (see IBC survey results)

Here’s a look at how MGAs are able to deliver

- One stop shop – MGAs that contract with multiple (re)insurance partners are able to offer a broad array of coverage options.

- Dealing with the decision maker – Because MGAs have delegated underwriting authority, not only can they offer a range of insurance products, they also control the process. There is no need to defer to one or more insurers to put together even the more complex structured solution.

- Special solutions for special risks – MGAs that invest in developing strong technical underwriting expertise, especially in niche areas, can help brokers with difficult to place risk (i.e. new or uncommon risks).

- Digital strategy – MGAs are adopting technology to make operational processes, such as policy and claim management, more efficient.

Key takeaways

- A managing general agent is an agency that is contracted to do business on behalf of (re)insurers

- Insurers delegate authority to MGAs to underwrite, bind cover, handle claims and perform other administrative tasks

- Delegated authority gives the MGA power to make decisions (i.e., underwriting) within pre-approved parameters.

- Insurers leverage MGAs for entering new markets and new geographies and to reduce costs

- An MGA’s duty is to the insurer, while a broker’s fiduciary duty is to the insured.

- MGAs play an important role in facilitating and enhancing insurance distribution.

Want to learn more?

Canada – Canadian Association of General Managing Agents

UK – Managing General Agents Association

USA – Wholesale and Specialty Insurance Association (formed in 2017 following the merger of the American Association of Managing General Agents and the National Association of Professional Surplus Lines Offices.)