This article explains the Claims Made vs Claims Made and Reported rules for claims reporting; how they work and what to watch out for in your insurance policy.

Claims Made vs Claims Made and Reported – understanding the difference

A Claims Made policy form offers coverage for claims made against the insured during the policy period. These policies typically come with a reporting requirement defined as “as soon as reasonably practicable.” This policy is also known as the “Pure Claims Made” policy.

A Claims Made and Reported policy form offers coverage for claims made against the insured during the policy period (just like the claims made form) and reported to the insurer during the policy period. In a Claims Made and Reported form, the reporting period is tightly defined, rather than left as “as soon as practicable.”

The key distinction between policy types involves the amount of time the insured has to report a claims. Under a Claims Made policy, the Insured has a longer period, extending beyond the policy term, during which a claim can be reported. Such policies will often use “as soon as practicable” language when defining reporting requirements. In contrast, the ability of an insured to report a claim under Claims Made and Reported policy ends on the expiry date of coverage.

The claims reporting requirements under Claims Made and Claims Made and Reported policies also apply to reporting circumstances that may give rise to a claim.

Which buyers should be aware of this distinction?

Policies typically offered in a Claims Made or Claims Made and Reported include:

- Directors & Officers Liability

- Employment Practices Liability

- Fiduciary Liability

- Cyber Insurance

- Errors & Omissions/Professional Liability/Professional Indemnity policies

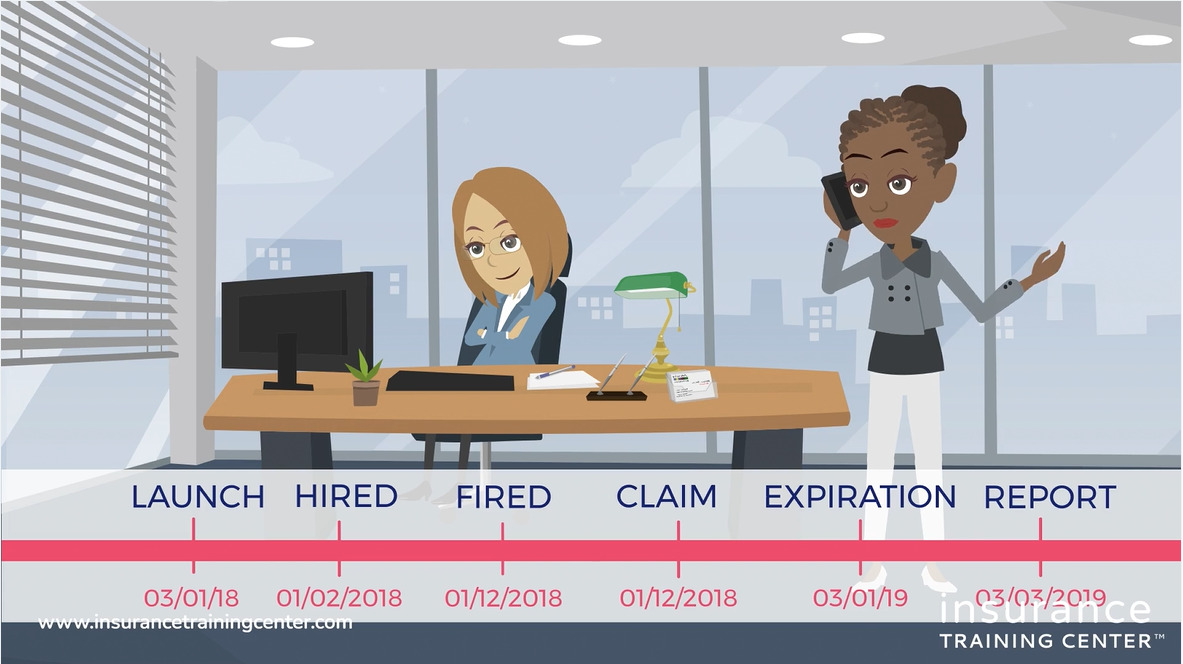

An example:

ABC Inc. was launched on January 1, 2018 and bought an Employment Practices Liability policy on that day:

- The policy contained an Effective date of January 3rd, 2018.

- The policy period was January 3rd, 2018 to January 3rd, 2019.

- February 1st, 2018 – ABC hired John Doe

- December 1st, 2018 – John Doe was fired

- December 31st, 2018 – ABC received a written demand from John Doe for wrongful dismissal.

On Claims Made and Reported forms, the claim must be reported within the policy period or as prescribed on the policy form. A claim made and reported form means much less freedom. However, it does provide more clarity. You have a precise window of time in which you can report a claim -otherwise, you run the risk of a coverage denial.

If we use the same example as above, the claim was made against the insured during the 2018-2019 period; then the claim also needs to be reported during that period.

If you are thinking, okay, that’s fine, but what if the claim happened on December 31 and policy renewed January 3! Do not panic; typically, you’ll see a month or two window (after the end of the policy period) to allow time should the claim arise at the end of the policy.

Is my policy Claims Made or Claims Made and Reported?

You can identify whether it’s a Claims Made form by reading the insuring clauses. To identify whether the form is a Claims Made form or Claims Made and Reported form, if it’s not stated in the insuring clauses (it’s often not), then you’ll want to look at the notice or reporting condition in the policy.

A Claims Made form states the policy covers claims made against the insured during the policy period. You might also see mention of coverage not being deprived unless the insurer has been prejudiced by the late reporting.

Often you find Claims Made and Reported policies disguised as Claims Made policies. These policies may say “Claims Made policies” on the declarations page or near or above the insuring clauses. However, in the reporting or notice section of the policy, there is a reporting timeline that is usually during the policy period and some small allowance after that, typically 30 or 60 days.

Key takeaways:

-

Knowing what basis a policy is on is one of the most important things to note about an insurance policy.

-

A Claims Made form and Claims Made and Reported form have different claims reporting implications

-

Talk to your broker or agent before canceling or non-renewing your insurance. Ask questions about coverage basis and coverage for claims brought forward in the future.

-

Talk to your broker or agent before switching policies. Understand the coverage basis of past and future policies before making changes, particularly from Claims made to Occurrence basis.

More…

- Extended Reporting Period Explained

- Occurrence vs. claims made policies explained

- Understanding Run-off Insurance