Derivative claims create one of the most important coverage issues in Directors and Officers (D&O) insurance: indemnification may not be available.

When shareholders sue directors or officers on behalf of the company, the corporation may be legally prohibited from indemnifying settlement payments. In these situations, directors and officers must rely on Side A D&O coverage for protection. For insurance brokers and buyers, understanding how derivative claims work and how indemnification applies is essential. These cases can involve significant legal costs, complex settlements, and personal liability exposure for corporate directors. This article explains:

- what derivative claims are

- how derivative lawsuits arise

- why indemnification works differently

- how D&O insurance responds

What is a derivative claim?

A derivative claim refers to the allegation of wrongdoing brought on behalf of a corporation against its directors, officers, or other insiders. The claim belongs to the corporation, but shareholders pursue it when they believe the company’s leadership has harmed the business and the corporation itself has failed to take action. Typical derivative claims include:

- Breach of fiduciary duty

- Mismanagement

- Fraud or unlawful conduct

- Insider trading

- False or misleading financial statements

- Waste of corporate assets

- Self-dealing or unjust enrichment

In insurance language, a derivative claim often refers broadly to a claim against directors or officers that arises from a shareholder derivative action and may trigger coverage under a D&O policy.

Derivative demand vs. derivative suit

A derivative suit (also called a derivative action) is the lawsuit shareholders bring on behalf of the corporation against its directors, officers, or other insiders. The term “derivative” reflects the fact that shareholders are deriving the corporation’s right to sue. Because corporate leadership controls the company, the corporation may not act against its own directors. In these situations, shareholders can step into the corporation’s place and pursue legal action.

Before filing a lawsuit, shareholders usually must submit a derivative demand to the board of directors. A derivative demand asks the board to:

- investigate alleged misconduct

- take corrective action

- bring a lawsuit on behalf of the corporation

If the board refuses the demand or fails to act, shareholders may then proceed with a derivative lawsuit.

Parallel derivative and oppression actions

In some cases, particularly in closely held corporations, a shareholder may bring both a derivative action and an oppression claim based on the same underlying conduct.

A derivative action seeks recovery on behalf of the corporation for harm done to the company. An oppression action, by contrast, seeks a remedy for personal harm suffered by the shareholder, such as conduct that is oppressive, unfairly prejudicial, or unfairly disregards the shareholder’s reasonable expectations.

Courts may allow these claims to proceed in parallel when the alleged misconduct harms both the corporation and the shareholder personally. The Ontario Court of Appeal recently provided guidance on this issue in Clark v. Cen-Ta Real Estate Ltd. (2025).

Common sources of derivative claims

Directors and senior management owe a fiduciary duty to act in the best interest of the corporation.

Shareholders may bring derivative claims when they believe leadership has breached those duties through actions such as:

- Breach of fiduciary duty

- Fraud or unlawful activities

- Insider trading

- Misleading or false financial statements

- Waste of corporate assets

- Self-dealing or unjust enrichment

Example of a derivative action (Alphabet)

In a high-profile example, shareholders of Alphabet, Google’s parent company, filed a lawsuit alleging that senior executives covered up a long-standing pattern of sexual harassment.

Alphabet agreed to establish a $310 million diversity, equity, and inclusion fund as part of the settlement of shareholder derivative litigation related to allegations that company leadership mishandled sexual misconduct claims against senior executives. The settlement, approved in 2020, is among the largest shareholder derivative settlements arising from #MeToo-related corporate governance claims.

The court explained the purpose of the settlement:

“Because the Settlement involves the resolution of derivative actions, which were brought on behalf of and for the benefit of the company, the benefits from the settlement will go to Alphabet. Individual Alphabet stockholders will not receive any direct payment from the Settlement”

– Notice of Pendency and Proposed Settlement of Derivate Actions

This highlights a key feature of derivative actions: the corporation, not the shareholder, receives the benefit of the settlement. Moreover, the court is very clear on how the proceeds of the settlement are to be used by the corporation:

“In order to provide appropriate funding for the Workplace Initiative, Alphabet shall cause to be spent a total of $310 million over the course of up to 10 years starting the first full fiscal year following the effective date.”

More recently, Alphabet also agreed to resolve a separate shareholder derivative lawsuit related to antitrust enforcement actions involving Google’s advertising business. In that case, the company committed $500 million over ten years to strengthen antitrust compliance and governance oversight. According to The D&O Diary, the settlement is one of the largest derivative settlements to date and illustrates how shareholder derivative actions often follow major regulatory investigations.

How D&O insurance responds

Directors and Officers (D&O) liability insurance protects corporate leaders from personal financial loss arising from lawsuits related to their management decisions. D&O insurance typically covers legal defence costs, settlements, and judgments. Coverage may appliy to lawsuits such as shareholder derivative actions.

A D&O policy usually includes the following insuring agreements:

- Side A coverage: Protects individual directors and officers when the company cannot indemnify them.

- Side B coverage: Reimburses the company when it indemnifies its directors and officers.

- Side C coverage: Provides coverage to the company itself for certain claims, typically securities claims against the corporation.

Wrongful vs. illegal acts

D&O insurance responds to alleged wrongful acts—like errors, misstatements, omissions, or breaches of duty. In derivative litigation, the alleged wrongful act often involves a breach of fiduciary duty.

However, D&O policies do NOT cover proven illegal acts. Coverage may still apply to defend allegations unless a final judgment determines that the conduct was deliberately fraudulent, criminal, or dishonest.

Derivative claims and indemnification

Indemnification is one of the most important insurance issues in derivative claims. In many lawsuits against directors and officers, the company indemnifies its leadership. The corporation pays the legal costs and settlements, and the D&O policy reimburses the company under Side B coverage.

Derivative claims are different.

In a derivative action, shareholders sue on behalf of the corporation. Because the corporation is considered the injured party, the lawsuit technically belongs to the company. This creates a legal problem. If the corporation indemnified directors for settlement payments in a derivative suit, it would effectively be paying itself. For that reason, many corporate laws restrict or prohibit indemnification for derivative claim settlements. For example, under Delaware corporate law, companies may indemnify directors for defence costs in derivative actions if they acted in good faith. However, the law generally does not allow indemnification for judgments or settlements paid to the corporation, because the company itself is the injured party.

As a result, directors and officers may face personal financial exposure for settlement payments in derivative lawsuits. In these situations, Side A coverage becomes critical, because it pays losses that company cannot indemnify.

Indemnification may also be unavailable when:

- the company is insolvent or bankrupt

- corporate bylaws restrict indemnification

- regulators prohibit indemnification in certain cases

Because of these limitations, derivative claims often rely heavily on Side A D&O coverage, rather than the more common Side B reimbursement coverage.

For brokers and insurance buyers, this distinction is critical. Derivative actions are a common source of large Side A losses in D&O insurance because settlement payments may be non-indemnifiable. Understanding how indemnification works and when it does not helps brokers structure D&O programs with appropriate Side A limits and protection for non-indemnifiable loss.

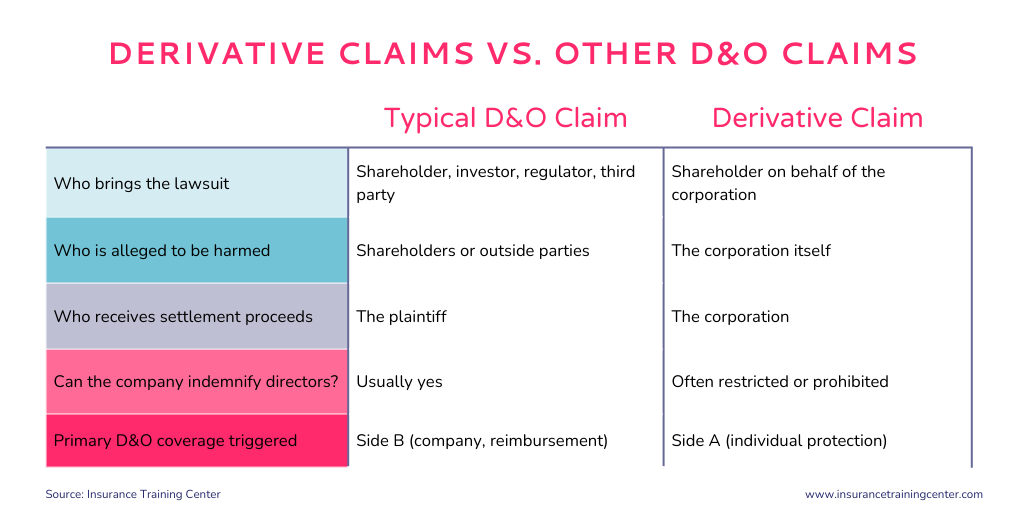

Derivative claims vs. other D&O claims

Not all claims against directors and officers work the same way. Derivative claims are unique because the corporation itself is considered the injured party.

Because indemnification is often limited in derivative actions, directors and officers may face personal financial exposure. This is why Side A coverage plays such an important role in protecting corporate leadership from derivative claims.

Case examples

Wells Fargo derivative action

Another large derivative settlement involved the Wells Fargo fake accounts scandal. Shareholders filed a derivative lawsuit against the bank’s directors and officers for failing to oversee sales practices that resulted in millions of unauthorized customer accounts. The case settled for $320 million.

Of that amount, $240 million was paid by Wells Fargo’s D&O insurers, making it the largest insurer-funded cash component in a shareholder derivative settlement at the time.

Yahoo

Yahoo shareholders filed a derivative lawsuit alleging that the company’s directors failed to properly disclose a massive data breach. The case settled for $29 million.

Cardinal Health

Shareholders sued the directors of Cardinal Health for allegedly failing to address risks related to opioid distribution. The derivative lawsuit resulted in a $124 million settlement.

Derivative investigative cost coverage

Many D&O policies include Derivative Investigation Cost Coverage. This coverage applies before a lawsuit is filed, when the company receives a shareholder derivative demand. A derivative demand asks the board to investigate alleged misconduct by directors or officers. Responding to the demand may require outside legal counsel, financial experts, or internal investigations.

Derivative investigation cost coverage reimburses the company for these pre-litigation investigation costs.

If the dispute later develops into a derivative lawsuit, the matter may then trigger the policy’s normal D&O coverage. At that stage, Side A coverage may become important if the company cannot indemnify its directors or officers.

Covered costs may include:

- legal counsel fees

- financial experts

- accounting investigations

However, this coverage has important limitations:

- It generally applies only when the company receives a shareholder derivative demand, and not to other types of claims, lawsuits, or regulatory investigations.

- It often carries a sublimit of about $250,000, which is frequently inadequate

- Excess D&O insurers usually do not extend coverage beyond the sublimit

Key takeaways

- A derivative claim is an allegation brought by shareholders on behalf of the corporation against its directors and officers.

- A derivative demand asks the board to investigate alleged misconduct before shareholders file a lawsuit.

- A derivative action (or suit) is the lawsuit shareholders file if the company fails to address the situation.

- Settlements in derivative actions benefit the corporation, not the shareholders who filed the lawsuit.

- Indemnification for settlements in shareholder derivative actions may be restricted or prohibited under corporate law.

- When indemnification is unavailable, Side A D&O insurance coverage protects directors and officers from non-indemnifiable loss.

- Many D&O policies also include Derivative Investigation Cost coverage, which helps pay for the costs of responding to a shareholder derivative demand.

Key terms in this article

Learn more…