Commercial crime insurance policies are available with two different claim reporting forms – 1) loss discovered or 2) loss sustained. This article explains what these mean, how they work, and their implications, so you can make an informed purchase decision.

Master Crime

Insurance.

It’s not a throw-in.

It’s a minefield.

Learn it before it matters.

What are ‘loss discovered’ and ‘loss sustained’?

‘Loss discovered’ and ‘loss sustained’ are claims reporting conditions in commercial crime insurance policies that define what needs to occur, and when, in order for claim coverage to be triggered. The key difference between the two is in the mechanism they use to activate coverage.

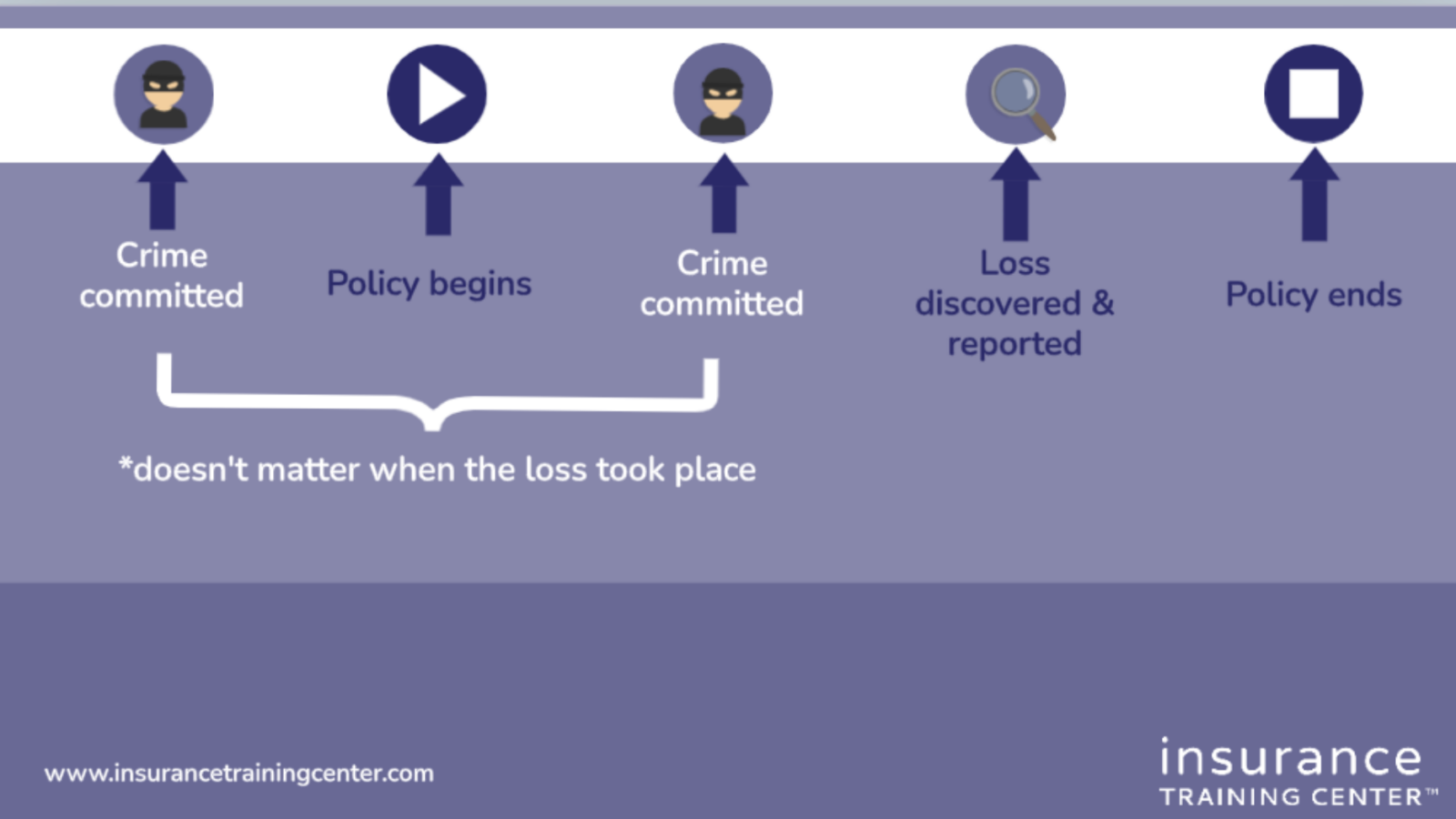

- Loss Discovered. A loss discovered policy requires that the loss be discovered and reported to the insurance company during the policy period. It does not matter when the loss took place. Learn more here.

- Loss Sustained. A loss sustained policy requires that the crime happen and be discovered during the policy period in order to be covered. If the loss happened before the policy period began, it may be covered IF the organization had crime insurance in place continuously and without lapse since that time. Learn more here.

When you go to purchase a commercial crime policy, your insurance broker may present you with the option of choosing between a loss discovered and a loss sustained policy. Whichever you select will have significant implications on if a loss is covered and if it is, the extent to which it is covered. Therefore, understanding the mechanics behind each approach is crucial before buying insurance or making changes to your policy such as transitioning from one policy type to another.

Commercial Crime Insurance

Commercial crime insurance is a type of property insurance that protects the insured organization by limiting the negative financial consequences it suffers from damage to, or destruction or disappearance of, its own property as a direct result of crime. This insurance only applies if the loss results from the man-made event of crime. It does not apply if property is damaged from a random weather event, or from an accident. Crimes perpetuated by employees or third parties can have far-reaching financial consequences for the affected organization. No organization is immune to crime.

Why timing is important

A particular challenge in crime insurance, is that with a crime, such as employee theft, there can be a lag between the time the employee starts stealing from the organization and the time the employer discovers the theft. And it’s only after the employer discoveres the crime that the organization can report the loss to the insurance company. This potential time lag complicates things. What if the crime began long before the insurance policy was purchased and the organization only became aware of it during the policy period? Should the policy cover the loss? Insurers need to have a means for determining where the boundaries are for coverage. Loss discovered and loss sustained are two different ways of setting those boundaries.

Important dates in a commercial crime insurance policy

| DATE | INSURANCE TERM |

| When the organization learned of the crime | Loss Discovered or Discovery Date |

| When the crime actually happened | Loss Sustained |

| When you informed the insurance company | Loss Reported |

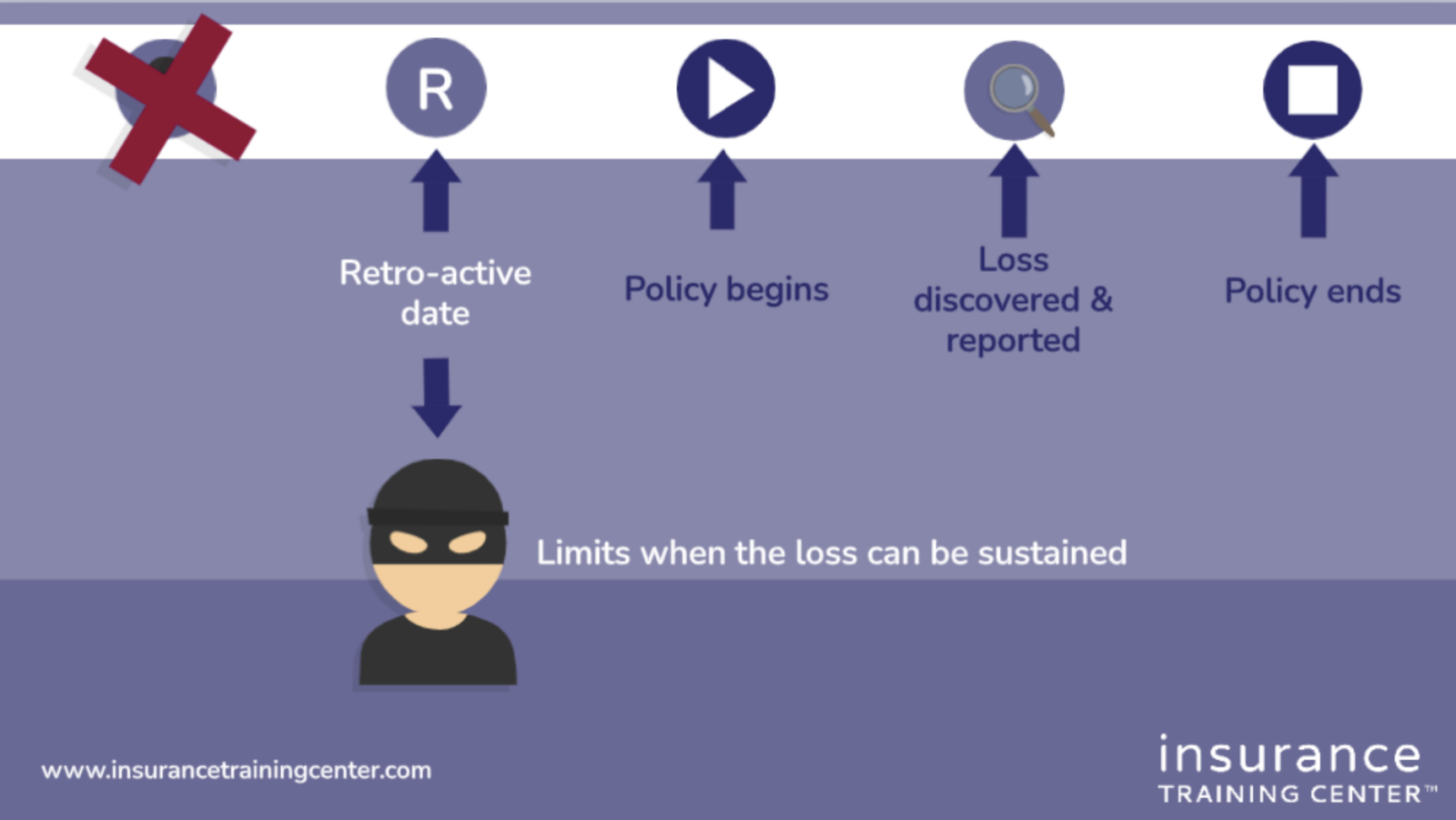

| The earliest loss date covered by the policy | Retroactive date (not all policies have it) |

As you can see in the above table, loss discovered and loss sustained refer to the date when the organization first learned of the crime and the date when the crime actually happened. These dates matter when filing a claim under a commercial crime policy. They are used to determine whether the insurer can cover your claim or not.

How does ‘loss discovered’ work?

A loss discovered policy provides coverage for losses discovered and reported to the insurer during the policy period. In a loss discovered policy, it does not matter when the loss took place. It only matters when the insured becomes aware of or discovers the crime.

The insured is obligated to provide a written notice to the insurance company immediately after the crime is discovered or, typically, no later than 30 to 60 days after the discovery of the loss. It is also mandatory for the insured to supply a proof of loss no later than four to six months after the discovery of the loss, depending on the policy.

Some loss discovered policies also have a date prior to the beginning of the policy called a “retroactive date”. This date limits policy coverage by excluding coverage for loss from crimes commited prior to that date. If a policy has a retroactive date, the insurance company will not cover a loss that the insured organization discovers during the policy period if the loss was sustained before the retroactive date.

A claim example:

Pay Less Supermarket purchased a commercial crime policy that ran from 1/1/20 to 1/1/21 with a retroactive date of 1/1/15. The policy contained a loss discovered claim reporting provision. Management discovered that an employee had embezzled $50,000, that was meant for operational expenses, dating back to March 14, 2019. The management submitted a proof of loss and received $50,000 back from the insurance company to cover the loss.

How does ‘loss sustained’ work?

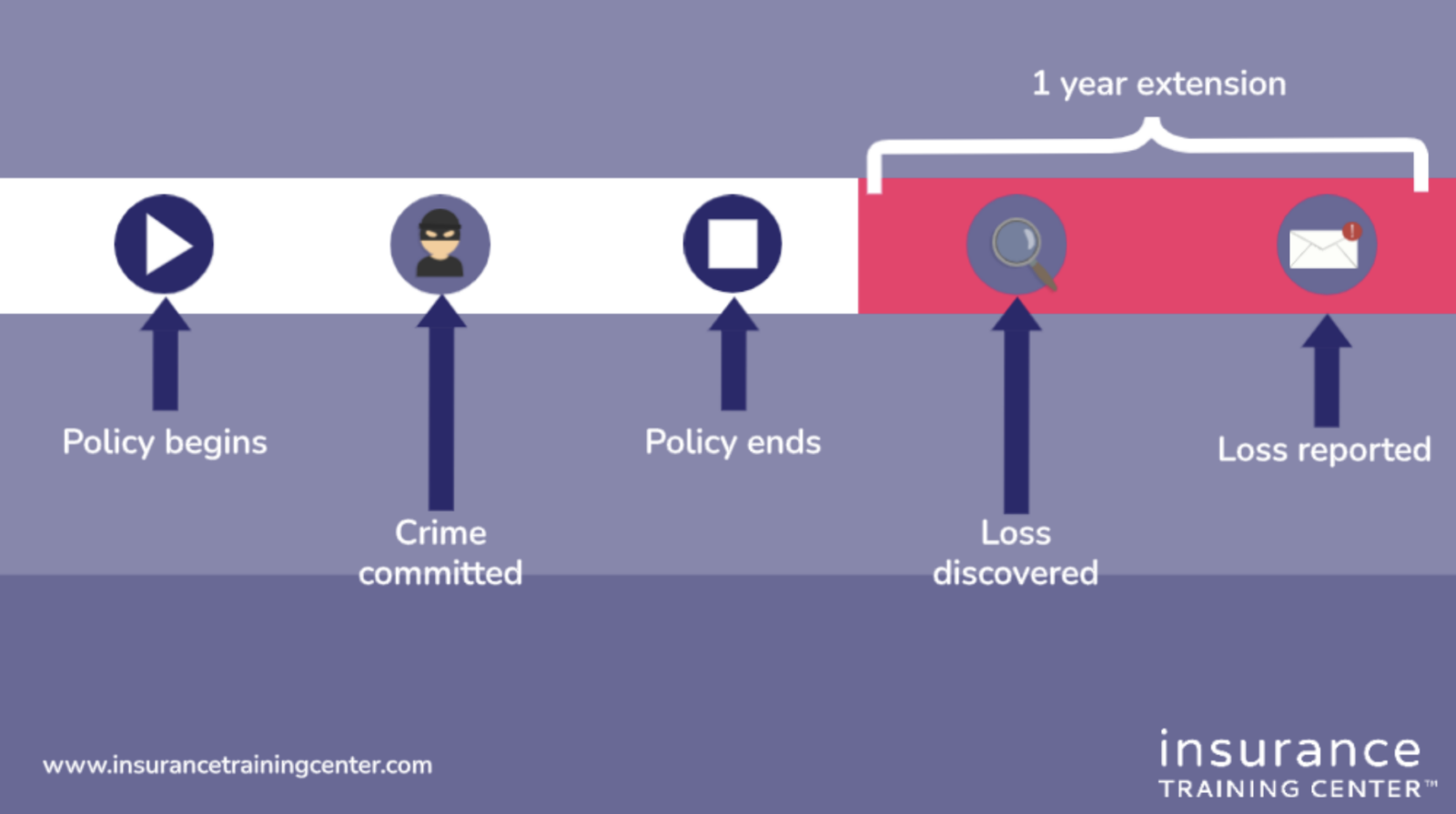

A loss sustained policy only insures losses that occur and are discovered during the policy period.

Earlier we discussed the challenge presented by the timing of events – crimes may go unnoticed for a long time before being discovered. According to the ACFE’s Occupational Fraud 2022: A Report to the Nations, a typical fraud case lasts 12 months before it is detected and some have lasted more than 5 years. (p13.)

A claim example:

A small business owner purchased a commercial crime insurance policy at the beginning of this year. An employee embezzled $55,000 in the previous year and the organization discovered the theft in April of this year. Because the theft did not take place during the policy period, it would not be covered by the policy.

With a loss sustained policy, a loss sustained before the policy period began is covered IF the organization has had crime insurance in place continuously and without lapse since that time.

If the insurance policy is terminated, for whatever reason other than non-payment, a loss sustained policy will also generally provide an extension of up to 1 year beyond the end of the policy period for the organization to discover and report a loss that was sustained during the policy period.

If you have an extended discovery period of one year, the policy could cover a loss that occurred during the policy period and discovered later. For example, if the loss happened between November 1, 2019, and November 1, 2020, but was only discovered in February 2021, it could still be eligible for coverage. While the policy covers only one year, with the extension, the insured has a longer reporting period.

Which to choose – loss discovered vs. loss sustained?

As an insurance buyer, determine which claims reporting rules you prefer for your organization. Ask your broker about ensuring that they structure your policy accordingly. Remember that the key difference between a loss discovered policy and a loss sustained policy is the event that triggers the coverage. A loss discovered policy provides insurance for losses that policyholders discover when the policy is in effect. While a loss sustained policy only covers losses that policyholders sustained and discovered during the policy period.

Organizations should aim for continuing with the same reporting rules from one policy period to the next to avoid potential issues such as gaps in coverage. You may elect to change policy terms because of a change in circumstances or, it could be that there is a change in what insurers are offering leaving the organization with no option but to make a change upon renewal.

If you switch from a loss discovered to loss sustained or vice versa, beware that there are coverage implications. Ask for guidance on the best way to structure your new policy to ensure continuity of coverage. We discuss this in greater detail in the Commercial Crime Insurance Fundamentals course.

Key Takeaways

- Insurance companies offer commercial crime policies based on either a loss discovered or a loss sustained approach

- ‘Loss discovered’ provides coverage for losses discovered and reported within the policy period, regardless of when they occurred.

- Alternatively, the ‘loss sustained’ policy option covers losses that occurred and were discovered during the policy period (with some exceptions).

- Coverage continuity should be a top priority when selecting loss discovered or loss sustained for your policy.